Brazil’s interest rate problem

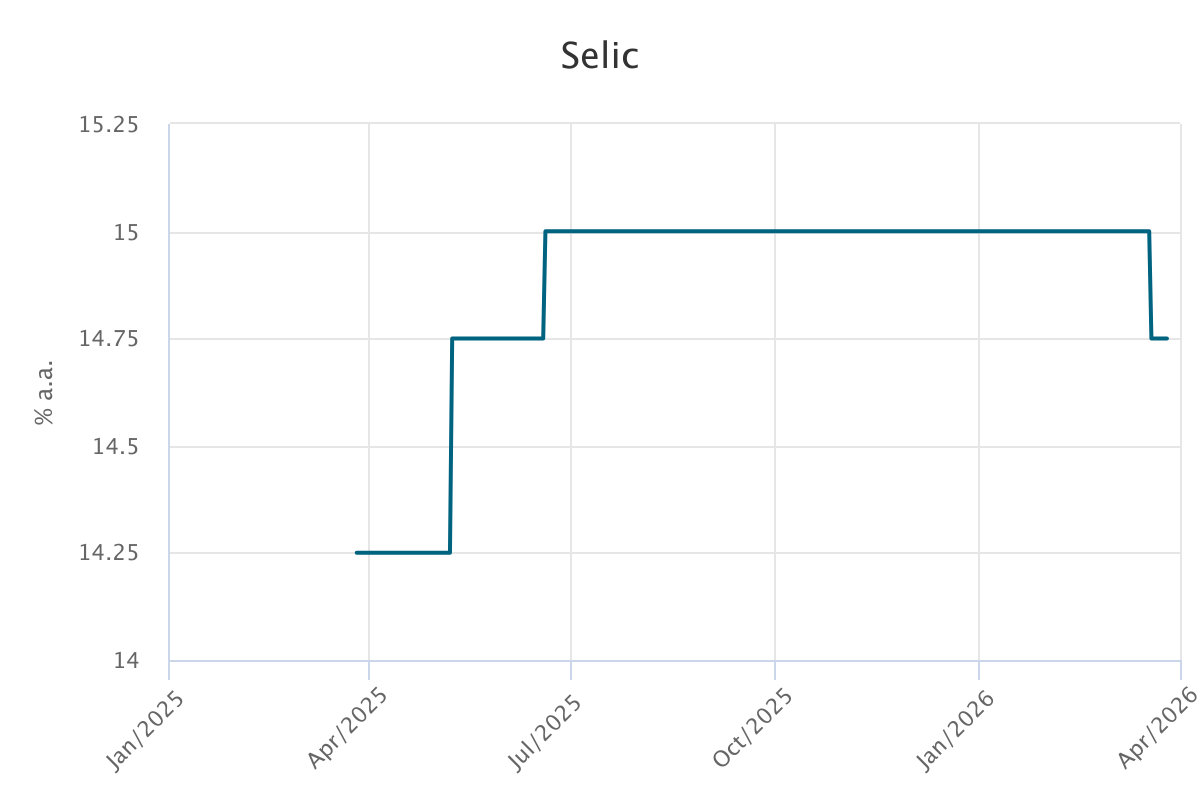

Recently, the Monetary Policy Committee (Copom) of the Central Bank of Brazil met to decide the target for the Selic rate for the next 45 days. The decision was to keep it unchanged at 15% per year—a choice with far from negligible implications.

Maintaining a benchmark interest rate at 15% in a context of declining inflation results in a higher ex ante real interest rate. Based on the latest data (the IPCA inflation rate for January at 4.4%), the ex ante real rate would stand at approximately 10.6%.

A more refined assessment suggests that whether the real interest rate is high or low should be judged relative to a benchmark—the so-called neutral rate of interest. The concept of the neutral (or natural) rate dates back to the seminal work of Knut Wicksell (1890). In contemporary terms, it is defined as the real interest rate that exerts no influence on inflation. In other words, if the real rate equals the neutral rate, monetary policy is neither stimulating nor restraining economic activity and, consequently, prices.

Recent estimates by the Central Bank itself indicate that Brazil’s neutral rate is around 5.5%. Against this backdrop, keeping the Selic rate at 15%, which implies a real rate of 10.4%, means that real interest rates in Brazil are approximately 4.9 percentage points above neutral. This reflects the degree of monetary policy contraction.

Had the Central Bank opted for a modest 25-basis-point cut at its previous meeting, monetary policy would still have remained in contractionary territory, albeit less intensely (around 4.7%). The issue, therefore, is not a change in the policy stance, but rather a recalibration. In its statement, the Central Bank justified its decision to maintain the nominal rate by highlighting two factors: (i) the resilience of the labor market and (ii) unanchored market expectations.

Starting with the first argument, by attributing its decision to keep rates high to labor market conditions, the Central Bank draws on the traditional literature surrounding the Phillips curve and its short-term trade-off between inflation and unemployment. However, the recent disinflation process has taken place despite the resilience of Brazil’s labor market. I raised this point in a recent column in Correio Braziliense, titled Inflation and the Labor Market. More recent refinements of the Phillips curve literature suggest that, under certain conditions, disinflation can occur without any cooling of the labor market. This appears to be the case in Brazil today. As such, the Central Bank’s concerns about labor market strength may reflect excessive conservatism.

The second point, however, is more problematic. Claiming that inflation expectations are unanchored based on median projections from the Focus survey may prove to be a mistake. In the first September report (05/09/2025), the median forecast for the IPCA stood at 4.85% for 2025 and 4.30% for 2026. The actual cumulative IPCA reading for December 2025 came in at 4.2%—well below forecasts made just three months earlier.

In short, the Central Bank effectively delivered in 2025 the level of inflation that had been expected for 2026 only months before. These data show that Focus projections have consistently lagged behind actual developments throughout the year. Calibrating monetary policy at its most contractionary level in 15 years based on such projections may therefore be a mistake—one with significant macroeconomic costs.

Another point that should be incorporated into this discussion is that Focus forecasts must be treated as endogenous. Put simply: why have these expectations systematically underestimated GDP growth while overestimating inflation? Is there anything the Central Bank can do—beyond maintaining excessively high interest rates—to better coordinate expectations?

In my view, the Central Bank could make greater use of communication tools—perhaps forward guidance—to counterbalance these projections. Put differently, does the Central Bank agree that IPCA inflation will reach 4.3% in 2026, or does it have arguments to challenge that outlook?

It is important to note that the Focus survey is constructed from aggregated median estimates and therefore incorporates divergent views. The Central Bank’s own assessment could play a crucial role in guiding expectations back toward anchoring. However, the monetary authority’s stance has so far been timid in this regard.

Ultimately, excessively high interest rates should not be normalized based on unanchored expectations that systematically fail to materialize ex post.

This article by Benito was published in Correio Braziliense just before the latest decision by the BCB to lower the Selic by .25 points.

| A guest post by

|

a sober article by Benito, which in addition to the 'neutral rate' in Brazil, raises important questions: Phillips curve, soft landing?, endogeneity of surveys and forward guidance..